According to the Global Banking Annual Review 2026, the global banking industry generated US$1.3 trillion in net income in 2025, up 7% from the previous year’s record, making banking the world’s most profitable industry once again. At the same time, McKinsey estimates that generative AI could create between US$200 billion and US$340 billion in annual value for the global banking sector through improvements in productivity and decision quality.

Those numbers explain why conversations around lending have become increasingly commercial rather than purely operational. When an industry of this scale looks for the next source of growth, even incremental improvements in credit quality, operational efficiency, and lending capacity become financially meaningful.

Consider an illustrative example. A financial institution managing a US$1 billion lending portfolio with an NPL ratio of 2.5% carries approximately US$25 million in non-performing loans. Improving that ratio to 2.0% would reduce non-performing loans to approximately US$20 million, a difference of US$5 million. While actual portfolios differ across institutions, the calculation illustrates why relatively small changes in portfolio quality can have a material financial impact.

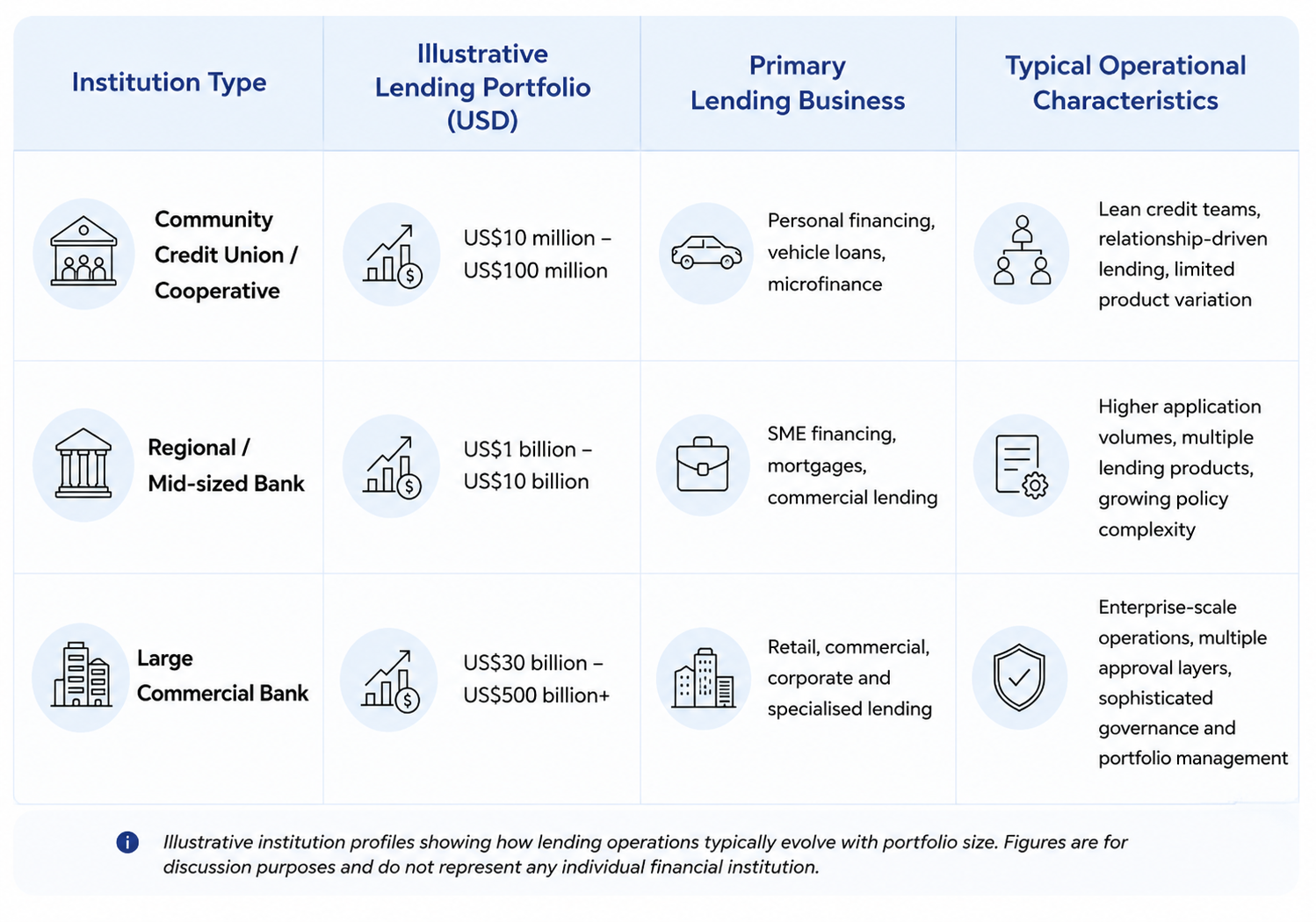

Credit Decisioning Looks Different at Every Scale

Every financial institution has its own lending strategy, customer segment, and growth ambitions. Yet regardless of size, lending operations often develop in remarkably similar ways.

The scale changes, but many operational patterns remain familiar. Product offerings expand, lending policies evolve, collateral structures become more diverse and exception handling gradually becomes part of everyday operations. Over time, credit teams spend less effort making the final decision than preparing information that everyone trusts before the decision is made.

Small Lending Decisions Shape Bigger Business Outcomes

One observation consistently emerges across lending institutions. Annual performance is rarely determined by a handful of large lending decisions. It is shaped by thousands of smaller decisions made every day.

An additional ten minutes spent validating borrower information may seem insignificant when reviewing a single application. Across 100,000 applications a year, that same activity becomes thousands of operational hours. Similar patterns appear in policy exceptions, collateral reviews, limit assessments, and repeated credit checks. Individually, they appear manageable. Collectively they influence turnaround time, operational expenditure, and, ultimately, lending profitability.

The same applies to portfolio quality. A modest improvement in NPL may look incremental on a quarterly report, yet its financial impact grows considerably when applied across multi-billion-ringgit lending portfolios.

Why Modern Credit Decisioning Engines Are Evolving

Investment priorities across financial institutions are gradually shifting towards improving the quality of lending decisions long before applications reach the approving authority. That shift is becoming increasingly visible across industry research, where AI is supporting lending operations through stronger document processing, more effective credit analysis, and better loan origination practices that reduce manual effort while improving decision quality across the credit lifecycle.

Modern Credit Decisioning Engines are becoming less dependent on individual capabilities and more dependent on how those capabilities work together. Structured borrower information, policy evaluation, collateral assessment, limit management, and explainable recommendations increasingly operate within a connected decision process, reducing repeated validation while improving consistency across lending operations.

The business impact is rarely measured by faster approvals alone. It becomes more visible through healthier portfolio quality, stronger operational efficiency, and greater lending capacity without proportional growth in resources.

AI Credit Decisioning Is Changing Lending Economics

Technology investment has always been part of banking, but conversations today increasingly begin with business performance rather than system functionality.

Portfolio quality, capital utilization, operational efficiency, and sustainable lending growth now appear in the same discussion as AI investment. That shift feels less like a change in technology strategy and more like a natural progression in how lending businesses evaluate long-term returns.

Every lending institution eventually arrives at a similar observation. The value of a lending operation has never depended solely on how many loans are approved. It depends on how consistently every credit decision contributes to healthier portfolios, stronger profitability, and more efficient operations.

The economics of lending rarely change because of one exceptional credit decision. They change because thousands of everyday decisions become just a little more consistent, a little more informed, and a little more connected. That is where the next generation of Credit Decisioning Engines is beginning to reshape the business of lending.

A net 0.5% reduction in your NPL ratio could recover approximately US$5 million for every US$1 billion in a lending portfolio, without approving a single additional loan.

Book a complimentary 30-minute Credit Decisioning ROI Review to discover how modern credit decisioning can help unlock measurable business value for your institution.