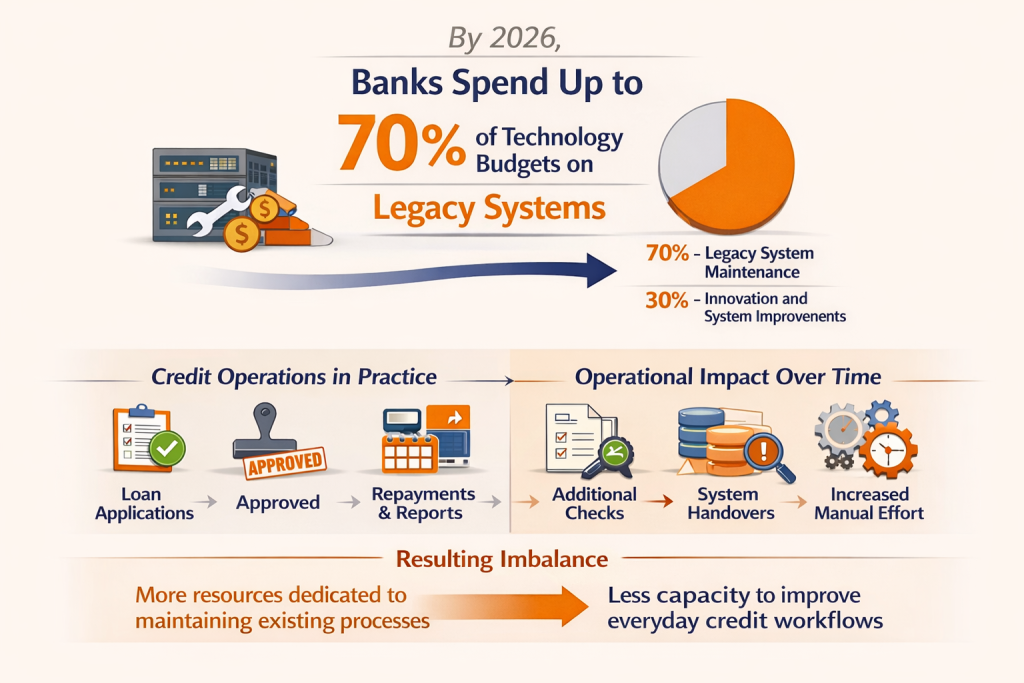

By 2026, industry analysis suggests that banks spend up to 70 percent of their technology budgets maintaining legacy systems, a reality that shapes how credit operations function in practice. Loan applications still move through established work

flows, approvals are issued within expected timelines, and repayments and reporting remain stable, but a growing share of operational effort is tied up in keeping existing processes running rather than making day-to-day credit work easier.

Where Manual Credit Effort Accumulates

In day-to-day credit operations, delays rarely sit with the approval decision itself, which is usually reached without difficulty; the time is absorbed by the work that surrounds that moment. Documents arrive in stages, information is presented in slightly different formats depending on the channel, and small changes to loan structures often trigger a sequence of follow-ups that were not planned for explicitly but are familiar to anyone involved in the process.

Credit officers manage this largely through experience, knowing which cases are likely to pass through cleanly and which will require closer attention, and having a shared sense of which checks genuinely matter and which exist largely because they have accumulated over time. This approach keeps operations moving, but it also means the process leans heavily on people who have seen enough cycles to recognize patterns early.

As volumes increase, that balance becomes harder to sustain. Work continues to get done, but it requires more coordination, more checking back, and more quiet intervention to keep things aligned, a shift that often becomes visible first during planning discussions, where timelines extend and even small changes take longer to assess than expected.

Pressure Builds Inside the Workflow Before It Reaches Reports

Across credit operations, the first signs of strain usually appear inside the workflow itself rather than in formal performance indicators. Exception queues grow because documents need one more check, turnaround times vary as credit operations absorb additional follow-ups, and priorities are adjusted informally to keep cases moving through the system. These changes are rarely flagged as issues at the time and are managed as part of normal operations.

When the patterns are reflected in reporting, they tend to appear as settled outcomes rather than developing conditions. Reports show where volumes landed, how long processing took on average, and which targets were met, but they rarely capture the additional effort required to keep those outcomes stable. As a result, growing manual load is often recognized only after it has become part of the operating baseline.

As lending environments become more complex and volumes less predictable, this delay matters more. The effort required to maintain steady credit operations increases quietly, while formal indicators continue to suggest that processes are under control. Over time, the gap between what credit operations manage day to day and what is visible at leadership level reduces the space to adjust early, when changes to workflow and coordination would be easier to absorb.

When Busy Turns into Constant Pressure

There is a difference between credit operations that are simply busy and those operating under constant pressure, a distinction most credit operations recognize through experience rather than metrics. Busy periods tend to pass. Sustained pressure gradually changes how work is done, with greater reliance on judgement, informal escalation, and manual handling because it is often faster than addressing underlying issues in the moment.

This shift becomes most visible during audits or portfolio reviews, when credit operations are asked to walk through how decisions were made and find themselves relying on memory, context, and the recollections of individuals who remember why certain calls were taken under specific conditions. While this reliance keeps operations moving, it also carries weight, keeping experienced staff closely involved and making it harder to scale credit operations without introducing additional manual effort.

At INFOPRO, we work with financial intuition to reduce the hidden operational load in credit without disrupting established discipline. If you are exploring how our credit intelligence suite can support steadier workflows and earlier insight in real operating conditions, we invite you to speak with our team to learn more.