Current industry data confirms the scale of the challenge facing the banking sector. As we move through 2026, many financial institutions still allocate a majority, often cited at around 70%, of their technology budgets just to maintaining existing legacy infrastructure. When most of the budget is locked into maintenance, the ability to respond to market shifts, such as real-time payment demands or automated compliance reporting, becomes significantly restricted.

In the banking industry, the discussion around technology often focuses on the final rollout, but the real work occurs years before that point. Transitioning or upgrading core banking systems is a high-stakes operational task. It requires balancing the urgent need for new functionality with the necessity of maintaining daily uptime. For a software provider, the goal is not just to deliver a product, but to ensure the institution’s central ledger remains a reliable foundation during periods of rapid change.

Managing the Accumulation of Technical Debt

A consistent pattern in long-term banking operations is the accumulation of workarounds. Over several decades, systems are often forced to perform tasks they were not originally designed for. For example, it is common to see a simple retail product launch require several layers of manual reconciliation because the underlying ledger cannot support modern interest accrual logic.

These issues are often overlooked until an institution attempts a significant integration. In practice, it is not uncommon to see API projects scheduled for one month extend into multiple quarters because the team had to decipher undocumented data fields repurposed decades prior. This is a practical example of technical debt in action. When legacy complexities are the primary factor in modernization efforts, they frequently fail to meet their original timelines or budget targets.

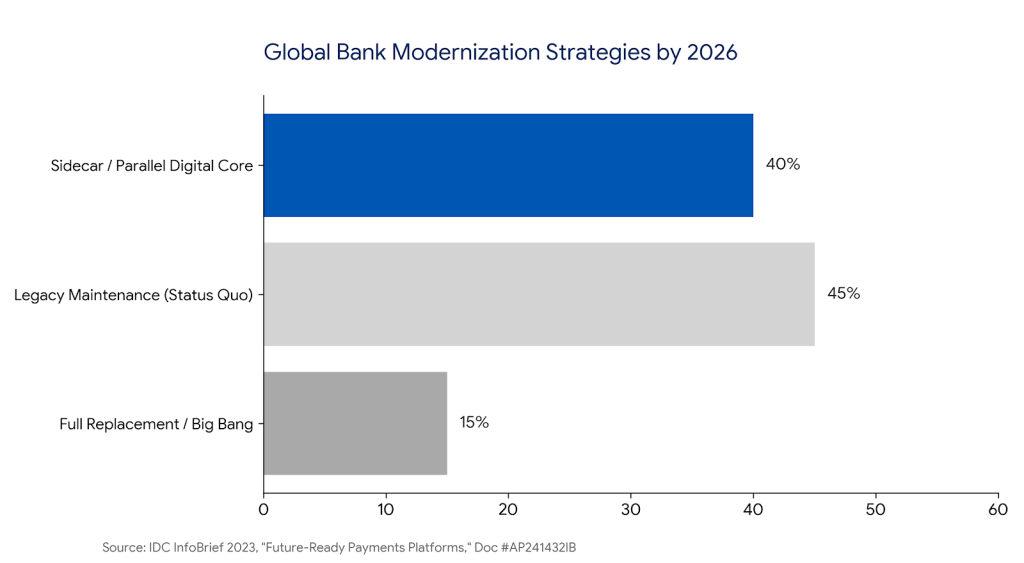

The Logic of Incremental Migration in Core Banking Systems

While the idea of a total “rip and replace” is frequently discussed in theoretical circles, it is rarely the most practical path forward for a tier-one or tier-two bank. The operational risk of a total cutover is usually too high for an institution of scale. The more successful migrations are those that occur incrementally, allowing for continuous validation of data and processes.

This methodology is becoming an industry standard. Data from IDC suggests that a significant and growing portion of global banks estimated at 40% are now utilizing “sidecar” strategies. This allows the institution to test new systems in a live environment without risking the entire book of business or interrupting daily settlements. This gradual shift ensures that the bank remains operational while the underlying technology evolves.

Utilizing the Orchestration Layer

One effective strategy involves focusing on the orchestration layer first. By migrating product logic and customer data into a modular framework, the legacy core is transitioned into a utility role. It continues to handle basic ledgering while the new architecture manages the “intelligence” and connectivity of the bank. This approach reduces the immediate pressure on the legacy system while building a path toward eventual decommissioning.

The Importance of Data Integrity

The most difficult part of any core transition is the data migration. Moving data from one table to another is relatively straightforward; however, preserving the integrity and context of that data is where the complexity lies. It is common to find legacy databases where specific fields were used for non-standard data storage simply because there was no alternative at the time.

A modern architecture requires clean, standardized data to function correctly. If the mapping is incorrect, the new system may process transactions, but the downstream effects on regulatory reporting and risk management can be severe. Most migration setbacks are caused by data quality issues rather than software defects. Addressing these issues early in the project is essential for long-term stability.

Reliability and Operational Discipline

A successful core banking system is defined by its reliability rather than its feature list. In a high-volume environment, the system must handle month-end processing and high-velocity API calls without latency spikes. Reliability is a quiet metric; when a system works perfectly, it is rarely a topic of conversation.

It’s found that the most resilient systems are those that prioritize a clean, simple underlying schema. By keeping the core focused on the fundamentals of ledgering, balancing, and audit trails, banks can achieve a more flexible environment. Research suggests that banks moving toward these modular architectures can, over time, achieve meaningful reductions in the 30 to 50% range in long-term application maintenance costs.

Ultimately, maintaining a competitive edge in 2026 is not about a single technology purchase. It is about the disciplined management of the core banking systems architecture to ensure it remains open, stable, and capable of supporting the next decade of growth.