In many financial institutions, the impact of AI lending operations is first noticed in routine workflow patterns rather than in performance reports. In one mid-sized lending environment handling both consumer and commercial portfolios, operational strain had gradually become part of daily work. Applications often required repeated verification, supporting documents came in varied formats, and approval timelines depended heavily on file complexity. None of these issues stopped production, but together they shaped how much coordination was needed to maintain steady output. It was within this setting that structured AI lending operations capabilities were introduced as a system layer rather than as a single tool.

How AI Lending Operations Become Structured with the SYNERGi AI Credit Intelligence Suite

When the SYNERGi AI Credit Intelligence Suite was introduced in this environment, the shift did not come from replacing existing infrastructure but from adding a coordinated intelligence layer across the lifecycle. The platform functioned as a structured processing framework that standardized how information entered, moved through, and exited each stage of evaluation.

Several functional components became visible through their operational roles:

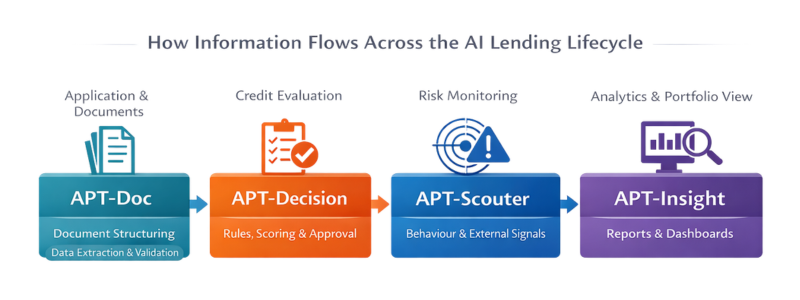

- APT-Doc: contextual document intelligence

Incoming applications and supporting files were analyzed automatically and converted into structured datasets. The module automates key processes such as document classification, quality and clarity checks, document values cross-checking, and the extraction of keys information from a wide range of document types. Instead of reviewing raw documents, teams received organized information ready for assessment, which reduced manual preparation and lowered the risk of missed details. - APT-Decision: unified decision logic engine

Eligibility rules, scoring models, and policy thresholds operated within one environment. Applications meeting defined parameters could proceed automatically, while high-risk cases were routed for review with relevant indicators already highlighted. Over time, this structure supported more consistent credit selection, improving overall loan quality and contributing to a steadier portfolio with lower non-performing loan (NPL) exposure. - APT-Scouter: external risk surveillance

Borrower exposure, behavioural indicators, and external signals were evaluated continuously rather than only during scheduled checks. Accounts showing early deviation from expected patterns were flagged automatically, allowing teams to assess them before conditions escalated. - APT-Insight: operational analytics interface

Portfolio indicators, approval distribution, and performance metrics were generated directly from system activity. Instead of compiling reports from separate sources, users accessed dashboards reflecting live lending conditions. Because outputs were drawn from structured execution data, reporting accuracy improved while preparation effort decreased.

What became noticeable in practice was not any single module but the interaction between them. Information structured at intake flowed directly into decisioning, decision outputs fed monitoring, and monitoring signals appeared immediately in analytics views. The process began functioning as a continuous system rather than a sequence of disconnected steps.

Operational Patterns Observed After SYNERGi AI Deployment

Over several processing cycles, workflow behaviour began to change in measurable ways. Application queues stabilized because fewer cases required clarification. Decision timelines became more predictable since baseline assessments were standardized. Monitoring activities shifted from periodic reviews to continuous visibility, allowing earlier identification of accounts requiring attention.

Seasonal volume increases provided another comparison point. Previously, peak periods required temporary adjustments in staffing or turnaround expectations. After the SYNERGi AI platform was integrated, similar volume surges passed with minimal disruption. Processing speed remained steady, suggesting that operational capacity had expanded without additional manual effort.

Audit preparation also reflected a practical difference. Because each validation step, rule trigger, and decision output was recorded automatically within the system, review trails could be retrieved directly rather than reconstructed from separate records. This reduced preparation time while improving traceability and consistency.

What This Reveals About AI Lending Operations in Practice

Observations across comparable lending environments suggest that the value of AI lending operations tends to appear first as operational stability rather than dramatic efficiency gains. Teams notice smoother transitions between stages, fewer repeated checks, and more consistent decision outcomes. These patterns indicate that the structure supporting daily work has become more reliable.

As these conditions persist, measurable indicators begin aligning with operational experience. Processing variability declines, reporting accuracy improves, and portfolio behaviour becomes easier to interpret because results are no longer shaped by inconsistent inputs. At that stage, improvements that initially felt subtle begin registering as quantifiable performance gains.

Conclusion

When AI begins structuring lending processes, the earliest evidence usually appears in workflow behaviour before it appears in performance metrics. Tasks move with fewer interruptions, information arrives ready for evaluation, and decisions follow clearer paths. Over time, these practical shifts accumulate into measurable results. In environments where this pattern develops, AI lending operations supported by platforms such as the SYNERGi AI Credit Intelligence Suite function not merely as automation tools but as operational foundations that enable consistency, visibility, and controlled growth across the lending lifecycle.