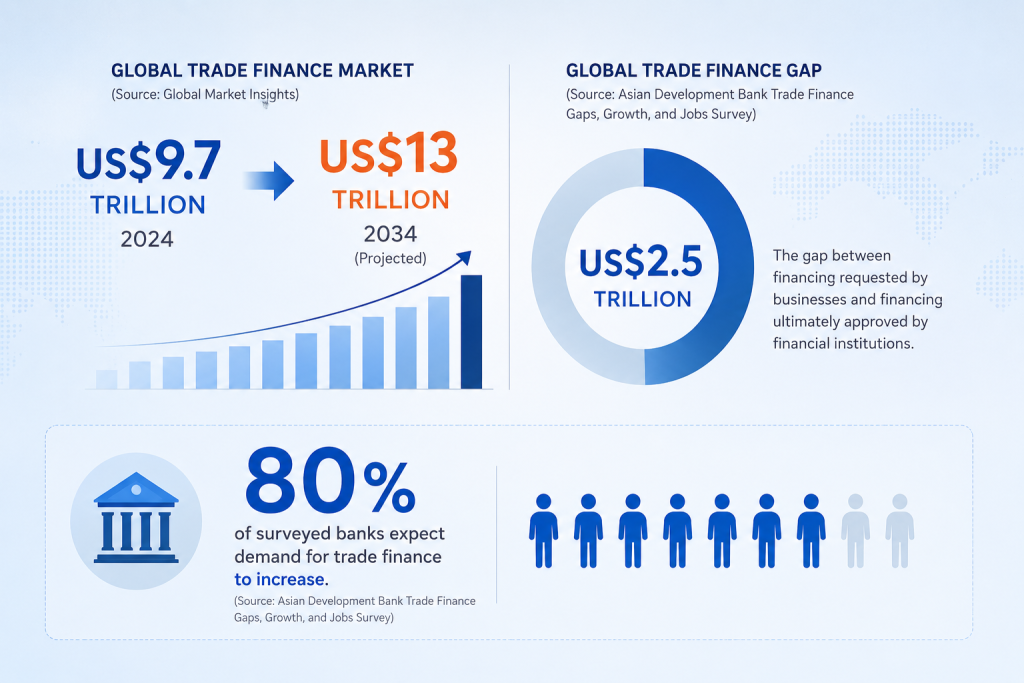

The global trade finance market was valued at approximately US$9.7 trillion in 2024 and is projected to reach nearly US$13 trillion by 2034 (Source: Global Market Insights). At the same time, the global trade finance gap remains at approximately US$2.5 trillion, reflecting the difference between financing requested by businesses and financing ultimately approved by financial institutions (Source: Asian Development Bank Trade Finance Gaps, Growth, and Jobs Survey).

As banks enter the second half of 2026, these figures are becoming more relevant in day-to-day operations. Businesses continue to diversify supply chains, expand into new markets, and seek financing support for increasingly complex trade relationships. According to the Asian Development Bank, 80% of surveyed banks expect demand for trade finance to increase as companies adjust their sourcing and trading strategies. Q3 is often the point where these trends become visible through transaction volumes, customer requests, and operational workloads.

Why Q3 Matters More Than It Appears

The middle of the year often marks a transition from planning to execution. Procurement programmes approved earlier in the year begin moving through supply chains. Manufacturers secure inventory for upcoming production cycles. Importers and exporters prepare for stronger trading activity in the months ahead. These developments create additional demand for letters of credit, bank guarantees, supply chain financing, and other trade-related services.

The impact is rarely concentrated in a single area. Activity increases across customer onboarding, transaction processing, documentation review, compliance checks, and settlement operations. Institutions gain a clearer picture of their operational readiness when these activities begin occurring simultaneously and at greater scale.

Global Trade Is Becoming More Complex as Market Dynamics Continue to Evolve

Businesses are increasingly managing relationships across multiple suppliers, jurisdictions, and logistics networks. New trade corridors continue to emerge while existing supply chains evolve in response to economic conditions, geopolitical developments, and market opportunities.

For banks, this creates a more demanding operating environment. Trade transactions frequently involve larger volumes of documentation, more counterparties, and greater requirements for visibility throughout the transaction lifecycle.

Many institutions have spent recent years strengthening their trade finance capabilities. Q3 provides an opportunity to observe how those investments perform under real operating conditions.

Corporate Customers Are Raising Expectations: Why Customer Relationships Matter More Than Ever

Corporate clients today expect timely updates, clear communication, and greater visibility into the progress of their transactions. Delays that once remained within operational teams increasingly affect broader commercial decisions, particularly when shipments, supplier commitments, and working capital requirements are involved.

Relationship managers often see this first-hand during periods of increased trade activity. Customers want confidence that transactions are progressing as expected and that potential issues can be identified early.

The institutions that consistently provide visibility and responsiveness tend to strengthen long-term client relationships through these interactions.

Readiness Is Often Revealed Through Everyday Operations

Operational readiness is rarely measured by a single project or initiative. It becomes visible through daily processes and decisions.

Transaction Visibility

Access to accurate and timely information allows teams to coordinate more effectively across departments. It also supports better customer communication when transaction updates are required.

Workflow Consistency

Trade finance transactions move through multiple stages involving documentation reviews, approvals, and risk assessments. Consistent workflows help maintain service quality as activity levels increase.

Risk Oversight

Growing trade activity often introduces additional complexity. Effective oversight enables institutions to manage exposures while continuing to support customer growth and international business activity.

The Questions Banks Are Asking Before Q4

As Q3 progresses, many discussions within trade finance departments focus on preparedness for the remainder of the year.

Common questions include:

- Can existing processes support increasing transaction volumes?

- Are customers receiving the visibility they expect?

- Do teams have access to the information required to make timely decisions?

- Can operational controls remain effective as workloads increase?

- Are current capabilities sufficient to support future growth?

These conversations often provide valuable insight into an institution’s ability to support customers through changing market conditions.

Looking Beyond the Quarter

The coming months will show how effectively banks support growing trade activity, respond to customer expectations, and manage increasing complexity across their trade finance operations. The lessons learned during this period will likely influence priorities well beyond year-end planning cycles.

As global trade continues its path toward a projected US$13 trillion market, trade finance readiness will increasingly be defined by an institution’s ability to deliver consistency, visibility, and control as demand continues to grow. Q3 2026 may prove to be one of the clearest indicators of which banks are prepared for the next phase of global trade.